Report Summary

Period covered: 03 May – 30 May 2026

3 minute read

Note: This report summary is one or two months behind the current month as standard reporting practice. The content is indicative only and incomplete with certain data undisclosed. Become a member to access this data or take out a free 30 day membership trial now.

Online performance

May was an exceptionally strong month for online retail. Online sales rose by xx% year-on-year, a sharp acceleration from the xx% decline recorded a year earlier and comfortably ahead of growth across the wider retail market.

Every online category recorded growth, with food and household goods leading the way. Clothing and footwear also enjoyed a strong month as warm weather arrived prompting seasonal purchases across apparel, footwear and outdoor living categories.

Online sales accounted for xx% of total retail sales, up from xx% a year earlier, while average weekly online sales reached £xx.

Key drivers

The joint third warmest May on record created immediate demand across summer clothing, sandals, garden products, fans, cooling appliances and outdoor leisure categories.

Online channels were particularly well placed to capture that demand through rapid fulfilment, broad product ranges and highly targeted promotional activity.

The strongest growth came from pureplay retailers. Non-store retailing sales rose by xx%, comfortably ahead of the xx% increase recorded by multichannel operators.

Consumers are spending more time researching products online, comparing prices across platforms and seeking out specialist retailers with wider assortments and stronger value propositions.

Retailer updates also pointed to improving digital engagement. Grocery retailers continued to invest heavily in loyalty ecosystems and app functionality, while operators such as AO and Kingfisher reported ongoing growth in digital traffic, marketplace activity and omnichannel engagement.

Macroeconomic backdrop

The economic environment became more supportive for online retail through May. Inflation held steady at xx%, grocery inflation eased further and oil prices fell back from the highs reached earlier in the spring.

Consumer confidence improved for the first time in four months, helping support discretionary spending across categories such as fashion, beauty and electricals. Measures of major purchase intentions remained weak, as households approached larger financial commitments cautiously.

Consumers remain willing to spend, but they are spending carefully. Digital channels are often the first place shoppers turn when comparing prices, researching products and identifying promotions. As households pay closer attention to value, online retail is benefiting from behaviours that naturally favour search, comparison and convenience.

The labour market also continued to cool, with vacancy levels falling and wage growth easing. Those trends have not yet translated into weaker online demand but are important indicators to monitor as the year progresses.

Take out a FREE 30 day membership trial to read the full report.

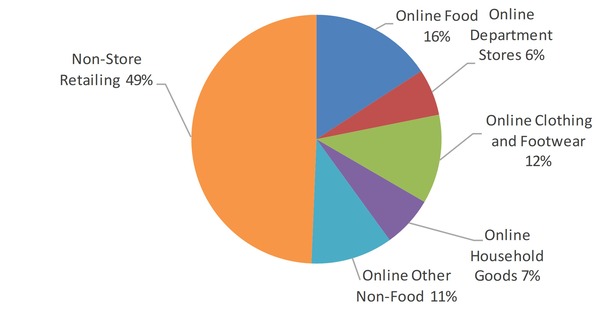

Proportion of online retail sales by category (Period aligned to ONS trading calendar – 3 – 30 May 2026 )

Source: ONS, Retail Economics analysis

Source: ONS, Retail Economics analysis